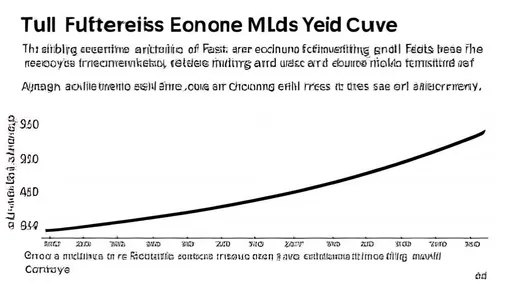

The recent flattening of the US Treasury yield curve, a phenomenon market participants refer to as a "bull flattener," has captured the attention of economists and investors worldwide. This specific dynamic, where short-term yields fall more rapidly than long-term yields or long-term yields rise slower than their short-term counterparts, is not merely a technical market movement. It often serves as a powerful signal, whispering clues about the underlying currents within the economy and the anticipated path of monetary policy. Interpreting these signals correctly is paramount for navigating the complex landscape of global finance.

At its core, a bull flattener typically emerges from a shift in market expectations toward a more dovish stance from the Federal Reserve. When economic data begins to show signs of softening—perhaps cooling inflation, weaker employment figures, or disappointing retail sales—traders start to price in the increased likelihood of interest rate cuts. This anticipation directly pressures the front end of the curve; yields on short-term Treasuries, which are most sensitive to changes in the Fed's policy rate, begin to decline. The market is essentially betting that the cost of borrowing money in the near future will be lower than previously expected.

Conversely, the long end of the curve tells a more nuanced story. While the short end reacts to imminent policy shifts, long-term yields are influenced by a broader set of factors, including long-term growth and inflation expectations. In a classic bull flattening scenario, the long end might also see yields decline, but at a much slower pace than the short end. This can happen because the same economic weakness prompting rate cut expectations also suggests subdued inflation and slower growth over a longer horizon, which naturally weighs on long-term yields. However, the key differentiator is the disparity in the rate of change between the two ends of the curve.

The message telegraphed by a bull flattener is often interpreted as the market forecasting a economic slowdown. It is a signal that investors are growing cautious about the immediate-term health of the economy and are seeking the safety of government bonds, particularly at the short end, thereby driving those prices up and yields down. This flight to quality is a classic risk-off move. It suggests a collective reassessment of growth prospects, leading to the expectation that the central bank will need to step in to provide support by lowering rates to stimulate borrowing and investment.

For the Federal Reserve itself, the evolving shape of the yield curve provides critical market-derived feedback. A bull flattener can be seen as the bond market validating the Fed's own concerns about economic growth or its efforts to combat inflation. If the Fed has been hinting at a potential pause or pivot in its tightening cycle, a move toward a bull flattener suggests the market is not only listening but is in strong agreement. It becomes a delicate dance between data dependence and market reaction, where the curve acts as a real-time barometer of confidence in the central bank's projected policy path.

The implications for various asset classes are profound and wide-ranging. For equity markets, the initial reaction to a bull flattener can be positive, as lower interest rates generally reduce the discount rate used in valuing future company earnings, making stocks more attractive. This is especially true for growth and technology stocks, which are more sensitive to financing costs. However, this positivity can be tempered by the underlying reason for the flattening—the anticipation of weaker economic growth, which could ultimately hurt corporate profits. The equity market often wrestles with this tension between lower rates and lower growth expectations.

Within the fixed income universe, a bull flattener creates a unique environment for portfolio managers. Duration positioning becomes crucial. Holding longer-duration bonds might seem less rewarding as their yields fall slower than shorter-duration bonds, but they still offer capital appreciation in a falling yield environment. Furthermore, the credit spread environment becomes tricky. While government bond yields fall, spreads on corporate bonds might widen if the economic outlook is dim, meaning the overall return on corporate debt could be mixed. This necessitates a careful, often more defensive, approach to credit risk.

It is absolutely vital to distinguish a bull flattener from its ominous counterpart, the bear flattener. A bear flattener occurs when long-term yields rise faster than short-term yields, often driven by the market pricing in rising long-term inflation expectations that could force the Fed to tighten policy aggressively. This scenario is generally seen as negative for both bonds and stocks. Confusing the two can lead to drastically incorrect interpretations of market sentiment. A bull flattener is born from expectations of monetary easing, while a bear flattener is born from expectations of monetary tightening or inflation fears.

While historically a reliable indicator, the predictive power of the yield curve, including the bull flattener, is not infallible. In the post-global financial crisis world, unprecedented monetary policy interventions like quantitative easing have distorted the traditional signals of the curve. Massive central bank purchases of long-term bonds have artificially suppressed long-term yields, potentially making the curve flatter than underlying economic fundamentals would suggest. Therefore, while a bull flattener is a significant signal, it must be analyzed in conjunction with a wide array of other economic data, from GDP reports and consumer price indices to global geopolitical developments.

In conclusion, the emergence of a bull flattener in the US Treasury yield curve is a multi-faceted development that demands a sophisticated understanding. It is primarily a story of shifting expectations toward a more accommodative Federal Reserve in the face of potential economic headwinds. For investors, it serves as a crucial cue to reassess risk, realign portfolios, and sharpen their focus on upcoming economic data and Fed communications. It is not a crystal ball, but rather a sophisticated language of the markets—one that speaks volumes about collective expectations for growth, inflation, and the very cost of money in the economy.

By /Aug 28, 2025

By /Aug 28, 2025

By /Aug 29, 2025

By /Aug 28, 2025

By /Aug 28, 2025

By /Aug 29, 2025

By /Aug 29, 2025

By /Aug 28, 2025

By /Aug 28, 2025

By /Aug 28, 2025

By /Aug 29, 2025

By /Aug 28, 2025

By /Aug 28, 2025

By /Aug 29, 2025

By /Aug 28, 2025

By /Aug 28, 2025

By /Aug 28, 2025

By /Aug 29, 2025

By /Aug 28, 2025

By /Aug 28, 2025